You're a leader within the community, an entrepreneur that faces risk head on, and a savvy business owner always looking for ways to make your company bigger and better with each passing day. You know that implementing a company-sponsored retirement plan is the next logical step, because, just for starters, it will help you attract and retain quality talent, reduce what you pay in taxes, and increase your own retirement savings. You just don't know where to begin. Well, it all starts with understanding the difference between a Defined Contribution Plan versus a Defined Benefit Plan.

Defined Contribution Plan

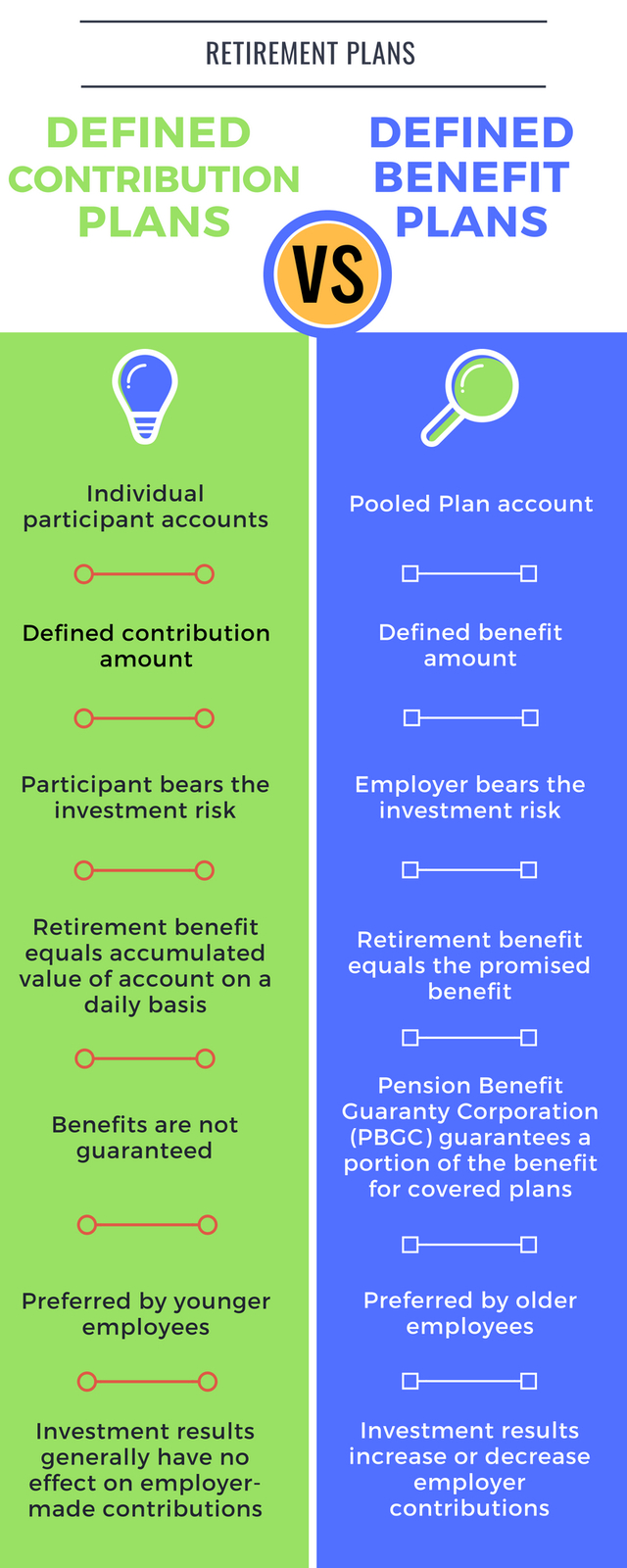

A defined contribution plan is sometimes known as an individual account plan. This is because the plan is a separate account that is maintained for each individual participant (e.g. 401(k)). These types of plans define the contribution amount (typically a percentage of the participant's pay) to be deposited into the participant’s account by each employee. Also employers may offer a company match or profit share contribution to participant's account plan as well.

As an example, a plan may provide that every eligible participant will receive an allocation or share of the total company contribution. However, this is highly relative to individual company-sponsored plan designs as they can be customized to meet the needs and goals of each business.

Defined Benefit Plan

A defined benefit plan promises to pay a specified benefit at a future retirement age (e.g. pension). Rather than stating the amount of money that an employee will put into an individual account, these plans define the amount of retirement benefit that will be paid to the employee by their employer at a future date.

The actual level of benefit is calculated using a formula stated in the plan document, which is the legal document that defines how the plan will be operated. The benefit is usually payable at a specified future date, such as when the employee/participant reaches the age of 65. Some retirement plans also provide benefits upon the disability or death of the participant before retirement.

See why businesses are demanding customized retirement plans

There are several pros and cons for each plan, dependent upon overall business strategies and goals. Though defined contribution plans have become exceedingly popular over the last few decades, there are many industries that still offer defined benefit plans (usually with older industries).

For your convenience, below is a quick comparison between the two plans for easy reference.

Quick Comparison Infographic!

For more tips and information regarding retirement plans, contact us.